The Blowback Machine: America’s War on Iran and the Ticking Clock

The US war on Iran was meant to prolong the life of the petrodollar. But can the US financial system withstand the global crisis it is creating?

This article is part of an ongoing series on the faultlines building beneath the U.S. financial system. Faultlines that are increasingly stressed by the U.S. assault on Iran.

The Convergence: When the External Shock Hits the Internal Fault Lines

The Dual Risk: Trapped Between Tokyo’s Tightening and the Semiconductor Supply Chain

The Gates are Closing: Private Credit’s Liquidity Crisis Deepens

The Blowback Machine: America’s War on Iran and the Ticking Clock

Introduction

“The United States has adopted a series of doctrinal documents, one of which proclaims that the US must dominate global energy markets,” Russian Foreign Minister Sergey Lavrov charged on May 13, accusing the Trump administration of seeking to “usurp” control over global energy flows and push Russian companies out of international markets.

Lavrov’s accusation is undoubtedly true. As previously discussed, a major motivation for the current U.S. war on Iran is to strengthen and prolong the life of the petrodollar by cementing control over energy supplies thereby eliminating rival currency challenges. But there is one important question the Kremlin’s foreign minister did not ask: Can the U.S. financial system withstand the global crisis it is creating?

The Architecture

The United States did not stumble into war with Iran. It chose it. The choice was decades in the making, born of a strategic calculation that a declining hegemon could reverse its trajectory by weaponizing control over the global energy supply chain, as explored in Economic Chemotherapy. The gambit was multilayered.

Ideally, Iran’s government would crumble and leave the path open for the dismemberment of the country and the looting of its resources. But that was, as we have seen in our review of the U.S. policy literature, always a long shot. Now the clock is ticking down to when the shock impacts U.S. geopolitical rivals.

This is the strategic bet. It is a bet that the short-term costs of war—the American lives, the military expenditure, the impact on American consumers, the diplomatic isolation—are outweighed by the long-term benefit of permanently—or at least, indefinitely—hobbling the economic rise of America’s geopolitical rivals.

But another clock is also ticking down. Counting down to a moment when the energy weapon the U.S. just fired starts to consume its own financial system.

The United States built the financial architecture of globalization as a power management system to extract value from the world. The core was deindustrialized. Production outsourced to the periphery. Supply chains geographically dispersed and differentiated to lock every node into the system. This architecture was designed to ensure the centrality of the U.S. consumer, U.S. markets and the USD.

This is the architecture the U.S. cannot insulate itself from. It is also the architecture that will ultimately transmit economic shocks to the financialized core.

As we will see, this is a financial core loaded with $5.3 billion in short bets against life insurers; $306 billion in unrealized bank losses; 2 trillion in opaque private credit underwritten by 1 trillion in net-asset value loans repackaged into opaque asset-backed securities.

The Illusion of Stability

The system was stable as long as three conditions held: cheap energy, cheap money and geopolitical quiescence. All three are now breaking. And they are breaking simultaneously, which is precisely what transforms manageable stress into a systemic test.

Cheap money has been the silent driver since the financial crisis of 2008. For nearly fifteen years, central banks across the West held interest rates at or near zero and pumped trillions of dollars of liquidity into global capital markets through quantitative easing. This did three critically important things. Firstly, it lowered the cost of servicing the enormous debt loads that governments, corporations, and households had accumulated.

Second, it ensured that the dollar, as the reserve currency at the center of this liquidity machine, faced no serious challenger, because no alternative currency offered a comparable yield or a comparable depth of safe assets.

But it did something else too. It generated a layer of opaque risk that is becoming difficult to ignore. By compressing yields on safe assets, it drove investors into riskier, more illiquid instruments—private credit, venture capital, real estate, and eventually the opaque structures that now sit on insurance company balance sheets.

That era is over. The inflationary shock of 2021-2023, a consequence of the pandemic-era policies, forced central banks to raise rates at the fastest pace in four decades. The Federal Reserve’s policy rate, which was near zero in early 2022, remains elevated in 2026. The European Central Bank, facing energy-driven inflation that it cannot control with monetary tools alone, faces an impossible policy dilemma: cut rates to support growth and import further inflation, or hold rates and watch the industrial base of the continent buckle under energy costs. The Bank of Japan, which has provided a hidden source of global liquidity for decades, is under pressure to normalize just as global liquidity is contracting.

The consequences of this shift are not merely that borrowing is more expensive. Much of the architecture of the current system—private credit funds, the insurance balance sheets filled with illiquid loans, a commercial real estate sector dependent on perpetual refinancing, sovereign debt loads manageable only at near-zero servicing costs—was only feasible in a monetary environment that no longer exists.

Cheap energy was the physical substrate. The globalized supply chains, the just-in-time manufacturing, the fertilizer-intensive agriculture, the containerized shipping that made it possible to produce goods in one hemisphere and consume them in another—all of it depended on oil and gas prices that did not reflect geopolitical risk. The Strait of Hormuz functioned. Russian gas flowed to Europe. The system assumed that the physical movement of energy would continue uninterrupted.

That assumption is broken. The largest supply disruption in recorded history is underway. Reports vary, but the World Bank's Commodity Markets Outlook confirms that initial global supply losses are estimated at 10 million barrels per day. The physical destruction of Gulf and Russian energy infrastructure is not a temporary logistics problem. It is the permanent degradation of the productive base.

Geopolitical quiescence was the political condition. The unipolar moment that followed the Cold War provided a security umbrella under which global trade could circulate freely. The United States guaranteed the sea lanes. The dollar served as the reserve currency. Rival powers were either integrated into the system or contained at its periphery. This condition has been eroding for years, but the open military conflict in the Persian Gulf, the kinetic degradation of Russian energy infrastructure by Ukraine, and the economic warfare between the US and China represent its definitive end.

The convergence of these three conditions is what really matters. Any one of these conditions breaking would be manageable. The system has absorbed energy shocks before. It has navigated interest rate cycles. It has endured geopolitical crises. But the simultaneous collapse of cheap money, cheap energy, and geopolitical quiescence is not three separate problems. It is a single structural event. The cheap money that allowed the servicing of debt and hid the accumulation of opaque leverage is gone. The cheap energy that powered the physical economy is gone. The geopolitical stability that underwrote the global trading system is gone.

So, the question is: Can the architecture that was built on a foundation of all three continue to function without them, and how do these shocks enter the system?

The Transmission Belt: How the Shock Enters American Finance

The first layer of transmission is the most direct. The American consumer, already buckling under the cumulative weight of inflation and a weakening labor market, is about to absorb a rear-loaded food-price shock—the counterpart to the front-loaded fertilizer-shock created by the closure of the Strait.

Purdue University’s agricultural economists estimate that a sustained energy-driven shock could add three to six percentage points to food-at-home inflation over twelve to eighteen months, with the first pass-through arriving three to six months after the fertilizer price spike.

The fertilizer shock began in March and April of 2026. Mathematically, the pass-through begins by mid-2026. The impact on northern hemisphere yields will start to become visible in autumn. The peak pressure on American grocery prices arrives in late 2026 and early 2027. This is not a foreign problem. This is an American household problem, and it will hit the bottom sixty percent of the income distribution hardest. This is when the financial system’s fault lines reach maximum stress.

The second layer of transmission runs through private credit and it is where the shocks begin to compound. The roughly $2 trillion private credit market—built on the promise of steady yields for retirees and savers—already faced a record 9.2 percent default rate in 2025, according to Fitch Ratings. Fitch noted that the nature of the loans left borrowers “highly vulnerable to elevated rates.” Redemption gates are spreading. Blue Owl, BlackRock, Apollo, Morgan Stanley, UBS: the names change but the mechanism is the same. Investors want their money back. The assets cannot be sold quickly without crystallizing devastating losses. So, the exit doors are being quietly locked.

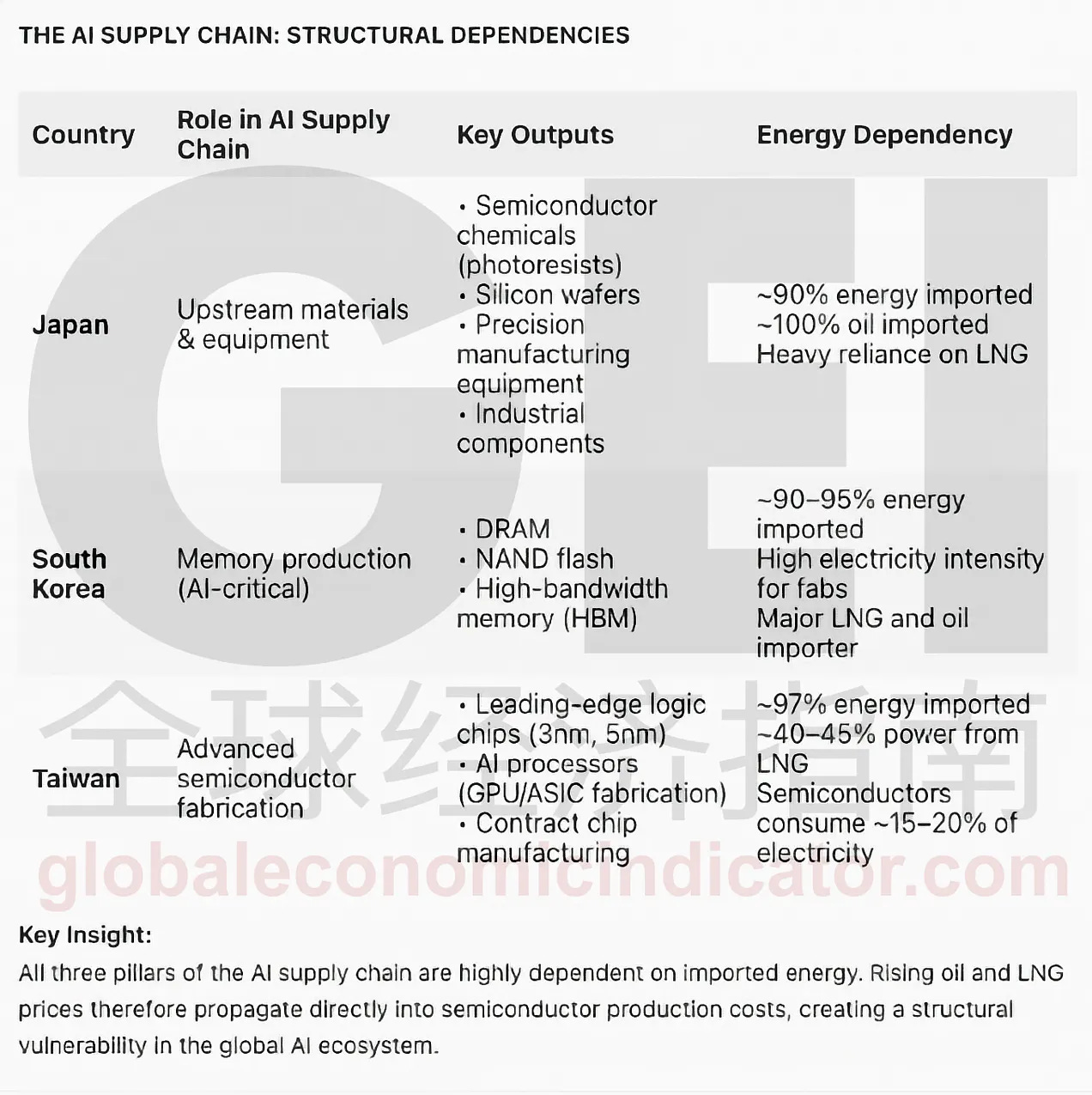

On of the reasons why defaults are rising in the private credit sector is because this is one of the points of contact where the AI boom meets the energy shock. S&P Global reports that planned 2026 AI infrastructure spending by Microsoft, Amazon, Alphabet, and Meta is estimated at roughly 635 billion, up from 383 billion the previous year and just $80 billion in 2019.

But semiconductor fabrication is energy-intensive, just-in-time, and geopolitically concentrated, specifically in Northeast Asia. S&P Global head of research Melissa Otto warns in the article that persistently high oil prices could force spending revisions, triggering a “really meaningful correction in all equity markets.” Companies that were supposed to benefit from AI infrastructure spending are finding their margins compressed and their credit quality deteriorating. These are the loans that sit inside the same private credit funds that are now facing a redemption crisis. AI is not just an equity bubble. It is a financing-chain problem of the first order.

The third layer is less visible but more systemic. This is how a crisis that starts in private credit creates contagion. It involves the way private credit funds finance themselves. To understand it, start with a simple example. A private credit fund lends money to companies. Those loans are hard to sell quickly because there is no exchange, no daily price, no ready buyer. But the fund itself sometimes needs cash, so it borrows from a bank, pledging its own portfolio of loans as collateral. This is called a NAV loan—a loan based on the fund’s net asset value.

Now, let’s go one step further. The bank that made that NAV loan does not necessarily keep it. It bundles a group of them together and sells them to investors—as an asset-backed security or ABS—who may have no idea they are ultimately exposed to loans that were already hard to value in the first place. This fund-finance market is now estimated to exceed $1 trillion. The risk is layered across the system: a company owes money to a private credit fund, which borrowed money against that loan, which was then packaged and sold to someone else. At every layer, someone assumes the asset beneath it is sound. But if the original borrower starts missing payments—because energy costs have crushed their margins, because the consumer has stopped spending—the chain of assumptions breaks. And because the underlying loans were never designed to be priced daily in an open market, no one knows what they are actually worth until someone is forced to sell. By then, the price discovery is catastrophic.

Life Insurers: The Risk Warehouse

If the private credit market is a risk transmission belt, the U.S. life insurance industry is the warehouse at the end of it.

Short bets against American life insurers have more than doubled to over $5.3 billion, according to Reuters analysis of data from ORTEX. These bets on life insurance stock were not made on hunches. They are not speculative attacks on random companies. The market is pricing a structural vulnerability created by the industry’s exposure to the private credit sector.

According to IMF and Moody’s data cited by Reuters, U.S. life insurers hold roughly 35 percent of their balance sheets in private lending, doubling over the past decade. The logic was straightforward: life insurers need long-duration assets to match long-duration policyholder liabilities. In a world of zero interest rates, private credit offered the yields that made the liability mathematics work. And because private credit does not mark to market daily, the volatility did not show up on the balance sheet.

But the assets are illiquid. The valuations are internal. The exposure, in many cases, is routed through captive insurance subsidiaries that a former insurance examiner quoted in the article, Tom Gober, estimates have absorbed roughly $1.54 trillion in transactions, operating with lighter disclosure and less regulatory scrutiny. And increasingly, the underlying loans are tied to the same AI-infrastructure credit risk driving the rise in defaults—Reuters explicitly notes this, stating investor concerns have been amplified by “questions over the value of the underlying loans, many of which have been made to AI infrastructure companies.”

The danger is not that insurers will collapse tomorrow. It is that they have become the largest concentrated holder of the hardest-to-price, hardest-to-sell credit risk in the U.S. financial system—at the precise moment when the energy shock that America unleashed is about to stress the borrowers behind those loans.

Annuity holders and policyholders are not institutional investors with gates and patience. They are American retirees who will need their money precisely when the cost of food and fuel is spikes. The question then becomes, what happens if this convergence triggers a wave of claims that insurers cannot meet without selling illiquid assets into a frozen market?

The Bank Layer: Stable Until It Isn’t

The banking system, for now, is not in crisis. On February 24th the FDIC reported in its fourth-quarter 2025 Quarterly Banking Profile that the industry finished 2025 in relatively good shape.

But the FDIC also noted that the industry continues to face “elevated unrealized losses” and “weakness in certain loan portfolios,” both of which “will remain matters of ongoing supervisory attention.” Total unrealized losses on held-to-maturity and available-for-sale securities portfolios stood at $306 billion as of year-end 2025. That was down from prior quarters, helped by a decline in mortgage rates that temporarily lifted bond prices. The FDIC cautioned that increases in longer-term interest rates would “likely reverse” those improvements. For now, the losses are parked comfortably on paper because no one has been forced to sell. But that comfort is conditional.

The same energy shock that raises food prices also raises default risk for corporate borrowers. As defaults rise, private credit funds face more redemption pressure. As redemption pressure increases, forced selling begins and asset prices decline. As asset prices decline, those $306 billion in unrealized losses begin to become realized. As they realize, the capital buffers that looked strong in a stable situation begin to look much thinner.

Banks are already pulling back from private credit financing lines. They are not doing this because they want to. They are doing it because they see the same risks accumulating and are hoarding capital to protect their own balance sheets. Less bank financing means harder refinancing for private credit borrowers. And that means more defaults. More defaults mean more redemption pressure. The feedback loop is not theoretical. It is already turning.

Beneath all of this lies another fault line: the slow, grinding collapse of the commercial real estate market. In March, Trepp reported the share of commercial property loans in default jumped to 7.55 percent. The alarming detail is what drove the increase. Roughly 40 percent of the newly defaulted loans had recently been marked as healthy—not because the buildings were thriving, but because the owners were still making payments while praying they could refinance before the loans came due. Then the loans matured. The refinancing fell through. The payments stopped.

The properties didn’t suddenly go empty. The money to roll the debt forward vanished. That is a credit-crunch signal, not a demand signal. And commercial real estate, like nearly everything else in this story, is heavily financed through the same private credit funds and complex financial structures now facing stress from every other direction. The damage migrates inward.

And Then There’s the Powder Keg

Everything described so far—the fertilizer shock, the private credit freeze, the insurer vulnerability, the unrealized bank losses, the CRE refinancing wall—is already in motion. These are not hypotheticals. They are documented stresses transmitting through U.S. financial architecture in real time.

But behind them sits a deeper accumulation of leverage that has not yet been tested. It does not require its own detailed analysis here. It simply requires acknowledgment, because if the stresses already in motion reach it, the scale of the problem changes by an order of magnitude.

The first layer is margin debt. As of early 2026, FINRA margin debt reached a record 1.28 trillion, marking nine consecutive months of increase and a 36 percent jump from the prior year. This is not just a record in absolute terms. Relative to GDP, margin debt sits at roughly 4.1 percent, nearly triple the fifty-year median of 1.5 percent. The net credit balance—cash in investor accounts minus margin loans—is negative $814 billion, meaning American investors collectively owe nearly a trillion dollars more than they hold in cash.

Margin debt, in and of itself, is not inherently dangerous but it carries a specific mechanical risk. When asset prices fall, brokers issue margin calls. Investors must either deposit additional cash or sell assets to meet them. Forced selling pushes prices lower, which triggers more margin calls, which forces more selling. This is not a theoretical dynamic. It is how every forced-liquidation cascade in modern financial history has unravelled. The rapid spikes in margin debt that preceded the downturns of 2000, 2007, and 2021 were not the cause of those crises. But they were the accelerant.

The second layer is the derivatives market. The Bank for International Settlements’ most recent triennial survey, conducted in April 2025, recorded a 27 percent increase in global foreign exchange derivatives turnover and a 59 percent increase in interest rate derivatives turnover compared to 2022, driven in part by the volatility shock from U.S. tariff announcements. The total notional value of over-the-counter derivatives likely exceeds a quadrillion dollars, concentrated in a small number of financial centers—primarily London and New York—and a small number of counterparty institutions.

The risk in the derivatives market is not the notional size, which is always staggering and always misleading. The risk is counterparty concentration. In a stable market, derivatives contracts net out. In a stressed market, a single major counterparty failure can transform a web of offsetting obligations into a cascade of broken claims. This was the mechanism that turned the Lehman Brothers failure from a single bankruptcy into a systemic seizure in 2008. The derivatives market has grown substantially since then.

None of this means a margin cascade or a derivatives event is imminent. It means the dry kindling is stacked higher than it was in the last cycle, and the sparks are already landing elsewhere in the structure. If the slow freeze now spreading through private credit, insurers, and CRE reaches this layer—if forced selling from redemption pressure triggers margin calls, if margin calls trigger broader asset sales, if a major counterparty stumbles under the weight of repricing—the phase change accelerates from slow to sudden.

This is the distinction that matters. The crises already unfolding are gradual, distributed, and opaque. The crises that margin debt and derivatives can produce are fast, concentrated, and spectacular. One tests the system’s ability to manage a slow drain. The other tests its ability to survive a sudden stop. The system may face both before this is over.

And that’s before we discuss the equity valuations of the Magnificent 7.

The Counterargument

A skeptic would say the following. The United States has endured energy shocks before. The 1973 oil embargo, the 1979 Iranian revolution, the 1990 Gulf War, the 2008 oil spike, the 2022 Ukraine shock: each time, the American economy bent but did not break. The Federal Reserve can cut interest rates until liquidity returns. The Treasury can guarantee money-market funds and backstop critical institutions. The financial system has circuit breakers. The architecture held before. It will hold again. Right?

The answer is that the financial architecture is different now. In each previous crisis none of the fault lines listed above existed, or to anywhere near the extent that they do today.

The circuit breakers were designed for a different machine. Interest rate cuts can ease financing conditions for solvent borrowers. They cannot rebuild the energy infrastructure that has been destroyed. Treasury guarantees can backstop money-market funds. They cannot make illiquid private credit assets liquid. The Federal Reserve can provide emergency lending to banks. It cannot prevent a consumer broken by food and fuel inflation from defaulting on obligations that sit inside insurance company balance sheets.

The relative-pain argument assumes the American financial system can absorb the shock without systemic damage. That assumption is what the fault lines call into question. If the energy shock triggers a cascading liquidity freeze across private credit, insurers, and banks, the damage cannot be measured in relative terms. An America in financial freefall is not stronger than a China in energy crisis: they are both in crisis. Unipolarity dies either way.

Can the System Hold?

So, we return to the central question: Can the foundations of the American financial system withstand the shock that its own government has chosen to unleash?

A system can absorb a single shock. It can absorb an energy shock, or a credit default cycle, or a redemption crisis, or an insurer solvency question, or a banking capital adequacy issue. What it cannot easily absorb is all of them arriving at the same time, amplifying one another.

When you lay the points of stress alongside each other things start to look worrying.

The fertilizer shock begins in the Gulf in March and April 2026. This passes through to American grocery shelves mid-2026. Harvest and yield effects become visible in autumn. The peak pressure on retail food inflation arrives in late 2026 and early 2027. Simultaneously, the private-credit default cycle, already at a record 9.2 percent, accelerates as corporate borrowers absorb the energy and food costs. Redemption gates spread across private credit and real estate funds. The fund-finance market faces its first significant markdowns on NAV-loan collateral. The asset-backed securities created from those loans begin to turn toxic but no one really knows what’s in them. Short bets against life insurers spike as concern grows about the valuation and liquidity mismatch of the assets on their balance sheet. CRE delinquency continues to slide sideways as defailts grow and refinancing failures driving new distress. Suddenly the banking system’s $306 billion in unrealized losses start to look very realized as forced selling accelerates.

These are not separate crises. They are the same crisis, from different angles, converging on a single timeline. The shock originates in a military decision made in Washington. It reverberates through the global energy and food system, through the architecture of globalization. It enters the U.S. financial system through the private credit market, the insurance industry, the banking system, the consumer household and the AI supply chain that runs from Northeast Asia. Each node is connected to every other node. The connections are the vulnerability.

The system is not definitely going to collapse. But it is facing a test for which it was not designed and for which its available tools are mismatched. The system was built on the assumption that energy would remain cheap, that money would remain free, and that the global architecture of American finance would continue to extract value from the world without transmitting that damage back home. All three assumptions are breaking simultaneously. That is not a prediction of certain failure. It is a statement that the probability of failure has risen to a level the system has never before faced.

The United States launched this war to break its rivals by wielding the energy weapon. It is now about to discover whether the weapon it built to dominate the world will destroy the financial foundations of its own power first. The blowback machine is running. It was made in America, one layer of opaque leverage at a time.

This article is part of an ongoing series on the faultlines building beneath the U.S. financial system. Faultlines that are increasingly stressed by the U.S. assault on Iran.

The Convergence: When the External Shock Hits the Internal Fault Lines

The Dual Risk: Trapped Between Tokyo’s Tightening and the Semiconductor Supply Chain

The Gates are Closing: Private Credit’s Liquidity Crisis Deepens

The Blowback Machine: America’s War on Iran and the Ticking Clock

This article is part of a series of analyses on the war against Iran. Other sections include:

Economic Chemotherapy: America’s Desperate Plan to Save Hegemony

The Strait Logic: Is the War on Iran a Dress Rehearsal for Blockading China?

The Petroyuan Trap: The U.S. Plan to Break China’s Economic Sovereignty

Petroyuan Trap Update: Fortifying the Dollar Perimeter

The Blowback Machine: America’s War on Iran and the Ticking Clock

References

Natural Gas Prices

Wall Street Journal (U.S. Henry Hub natural gas):

https://www.wsj.com/finance/commodities-futures/u-s-natural-gas-futures-pick-up-in-early-trade-45f2458fTrading Economics (EU TTF natural gas):

https://tradingeconomics.com/commodity/eu-natural-gasTrading Economics (Japan-Korea Marker LNG):

https://tradingeconomics.com/commodity/liquefied-natural-gas-japan-korea

Fertilizer and Food Prices

Reuters (Hormuz disruption and fertilizer squeeze):

https://www.reuters.com/world/china/iran-war-fertiliser-squeeze-could-spell-trouble-next-years-grain-harvests-2026-04-27/Reuters (India imports 2.5 million tons of urea at sharply higher prices):

https://www.reuters.com/world/india/india-import-record-25-million-tons-urea-nearly-double-price-paid-two-months-ago-2026-04-22/USDA Economic Research Service (Fertilizer costs and farm production expenses):

https://ers.usda.gov/sites/default/files/_laserfiche/publications/113324/ERR-354.pdf?v=89250Purdue University Center for Commercial Agriculture (Iran conflict and consumer food prices):

https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-and-consumer-food-prices-a-broad-but-lagged-and-sticky-shock/

Insurance and Private Credit

Reuters (Short sellers target U.S. life insurers over private credit concerns):

https://www.reuters.com/legal/government/short-sellers-bets-life-insurance-stocks-soar-private-credit-concerns-grow-2026-04-27/

Private Credit and AI Exposure

Reuters (Wall Street monitors private credit risk from AI disruption and outflows):

https://www.reuters.com/legal/transactional/wall-street-monitors-private-credit-risk-ai-disruption-outflows-cause-concern-2026-04-14/Reuters (Fund finance market reaches $1 trillion):

https://www.reuters.com/legal/transactional/fund-finance-market-reaches-1-trillion-driven-by-private-credit-moodys-says-2026-04-27/

Commercial Real Estate

Trepp (CMBS delinquency rate):

https://www.trepp.com/trepptalk/cmbs-delinquency-rate-jumps-in-march-2026

Banking System

FDIC Quarterly Banking Profile and remarks:

https://www.fdic.gov/news/speeches/2026/fdic-quarterly-banking-profile-fourth-quarter-2025

AI Capital Expenditure

Reuters (Big Tech’s $635 billion AI spending and energy shock):

https://www.reuters.com/world/china/big-techs-635-billion-ai-spending-faces-energy-shock-test-sp-global-says-2026-03-31/

Thank you! This is a particularly clear summary of a very complex topic. This financialisation of everything wreaks havoc on the whole world, and, if I understood your argument, it is now coming home to roost.

Ryan, again rilliant mapping of the AI-infrastructure,private-credit, insurer nexus. The market still treats AI as an insulated software trade, ignoring that data centers and fabs are essentially energy-arbitrage machines that are now geopolitically exposed.

With Trump rejecting the ceasefire and Hormuz choking ~20% of global LNG, EU TTF is climbing toward €46.60/MWh and Asian JKM is at $18.81/MMBtu. The immediate casualty isn't just the U.S. consumer, it’s the industrial capacity of U.S. allies in Europe and Asia.

You are absolutely right that the U.S. consumer will be crushed by imported goods inflation and global food/fertilizer parity. But for the U.S., this acts as a brutal internal wealth transfer to domestic energy and agri producers. For Europe and Asia, it is structural wealth extraction. This allied industrial distress is what will inevitably force the Fed to heavily activate Central Bank Swap Lines to prevent a global dollar funding freeze.

The Fed's swap lines can buy the system 12-18 months of liquidity time, but they cannot fix the solvency of the underlying credit collateral. Record margin debt is just the accelerant; the actual detonator is Private Credit Redemption Gates. When those gates lock, the $1T fund-finance market will violently reprice, directly blowing up the life insurer balance sheets you highlighted.

You are spot on. By choking Hormuz to hurt rivals, the U.S. is violating the foundational contract of its own petrodollar hegemony. The blowback machine is indeed running.